Table of Contents

Traders like gold for several reasons. Firstly, gold is viewed as a haven asset that retains value during economic and political uncertainty. It is also a hedge against inflation, as its value tends to rise when inflation rises. Secondly, gold is a highly liquid asset that can provide diversification benefits to a portfolio.

Lastly, the supply of gold is limited, and its price is influenced by supply and demand dynamics. This makes it attractive to traders who can take advantage of price movements. As a result, gold can be an attractive asset for traders looking to diversify their portfolios, protect against inflation, or exploit supply and demand dynamics.

Gold and global instability

Fitch has predicted a global recession in 2024. A recession is typically defined as a period of significant economic decline, marked by a contraction in economic activity, a reduction in GDP, and rising unemployment rates.

The projected GDP growth rate of 1.7% is considered slow and indicates that the global economy will likely face significant challenges in the coming years. The slow growth rate may be due to various factors, including ongoing global uncertainties such as geopolitical tensions, trade disputes, high interest rates, and several bank bankruptcies in the US.

A recession can significantly impact individuals and businesses worldwide, with job losses, reduced income, and lower levels of economic activity leading to financial instability and hardship. As such, individuals and companies need to take steps to prepare for and mitigate the impact of a potential recession, including diversifying their investments, reducing debt, and building up emergency savings.

Gold price today in the USA

Gold Price Prediction in 2026

Here’s a fundamentals-only read on gold using just the files you attached (US/UK CPI, policy rates, GDP, and trade balances). I pulled the 2025 trends and then rolled them forward into 2026 scenarios.

Based on 2025 fundamentals, gold is likely to rise moderately in 2026, up to $430,0 as the U.S. Federal Reserve continues easing and real interest rates fall closer to 1%, keeping demand for safe-haven assets strong. Unless inflation drops sharply below 2%, the most probable trend is a steady bullish move of 5–15% through 2026.

| Month | US_CPI_YoY | US_FED_Interest_Rate | RealPolicy | |

|---|---|---|---|---|

| 166 | 2025-01 | 2.9 | 4.5 | 1.6 |

| 167 | 2025-03 | 2.8 | 4.5 | 1.7000000000000002 |

| 168 | 2025-05 | 2.3 | 4.5 | 2.2 |

| 169 | 2025-06 | 2.4 | 4.5 | 2.1 |

| 170 | 2025-07 | 2.7 | 4.5 | 1.7999999999999998 |

| 171 | 2025-09 | 2.9 | 4.25 | 1.35 |

| 172 | 2025-10 | 3.1 | 4.25 | 1.15 |

(I also prepared a small table for you with the US 2025 CPI vs Fed rate and the implied real policy rate so you can inspect month-by-month alignment.)

Inflation vs. Policy (the core driver for gold via “real rates”)

-

US CPI YoY (avg 2025): ~2.72% (2024 avg in your file: ~3.00%).The latest point in your file (dated 2025-10-24) is 3.1% — an uptick late in the year.

-

Fed Funds (avg 2025): ~4.43% (2024 avg ~5.22%). Latest in your file (2025-10-29): 4.25%.

-

Implied US real policy rate (Fed − CPI): 2025 average ~+1.7%, slipping to ~+1.15% in the most recent print. Falling real rates are supportive for gold.

Growth (macro backdrop / “recession premium”)

-

US GDP “Actual” (your series) avg 2025: ~1.38 vs ~1.68 in 2024 → growth cooled in 2025 in your data.

-

UK GDP avg 2025: ~0.37 → sluggish growth.

External balances / Dollar context

-

US goods trade deficit avg 2025: ~−$93.6B per month (your series) — wider than 2024 (avg ~−$71.8B). A persistently larger US deficit is a medium-term headwind for USD, which is bullish for gold (all else equal).

-

UK trade deficit avg 2025: ~−£9.0B — also weak, but gold is far more sensitive to US real yields and the USD than to UK data.

Bottom line from your 2025 data:

-

The Fed eased (policy rate down) while US inflation stopped falling late in the year (last 3.1%).

-

This compressed real rates through 2025 — historically positive for gold.

-

Growth cooled, and the US trade gap widened — both macro supports for gold.

2026 outlook for gold (scenarios grounded in your 2025 trends)

Gold’s macro “lever” is the US real rate (≈ Fed rate − CPI). I’ll map scenarios by where that real rate likely sits in 2026 if 2025 dynamics continue.

Base case (most consistent with your 2025 trend)

-

Assumption: Fed trims a bit more or stays ~4.0–4.25% through mid-2026; CPI runs 2.5–3.0% on average (your late-2025 tick-up persists but doesn’t surge).

-

Real policy rate: ~0.75%–1.25% (down from ~1.7% avg in 2025; near your latest ~1.15%).

-

Implication: Real-rate drift lower + soft global growth + wide US deficit → gold biased higher.

-

Call: Moderately bullish — think +5% to +15% over 2026 vs current levels (directional band, not a price target).

Bull case (re-inflation / soft-landing cut mix)

-

Assumption: CPI holds ~3.0–3.5%, the Fed doesn’t (or can’t) keep the policy rate much above ~4%, and growth stays mediocre.

-

Real policy rate: ~0.0%–0.5%.

-

Implication: Real yields near zero historically fuel stronger gold up-moves; US deficit adds tailwind; risk hedging stays in demand.

-

Call: Bullish — +15% to +25% in 2026.

Bear case (disinflation outpaces cuts)

-

Assumption: CPI glides to ~2%, Fed holds ≥4% (or signals higher-for-longer into 2026).

-

Real policy rate: ~1.5%–2.0% (back up toward your 2025 average).

-

Implication: Higher real rates pressure gold; dollar steadies despite the deficit.

-

Call: Bearish — −5% to −10% in 2026.

How each attached series feeds the view

-

US CPI ↔ Fed rate → Real rate (primary): Your data shows 2025 cuts and a late CPI uptick, compressing real rates into year-end — classic gold-positive setup if it persists.

-

US GDP: 2025 cooling reduces the Fed’s room to keep real rates high ⇒ supports gold.

-

US trade deficit: A larger average deficit in 2025 weakens the medium-term dollar narrative ⇒ supports gold.

-

UK CPI/Rate & UK GDP: Helpful global color, but secondary to the US real-rate channel for gold.

Risks to the view

-

Disinflation surprise to ~2% while the Fed stays ~4%+ → real rates rise, gold headwind.

-

Sharp growth rebound (US GDP re-accelerates) → stronger USD, gold headwind.

-

Geopolitical relief → safe-haven demand fades, gold headwind.

-

Conversely: renewed shocks (energy, geopolitics, credit) that lift CPI or force faster cuts → gold tailwind

Gold’s current spot price hovers around $3,845 per ounce, and based on 2025 fundamentals — falling real interest rates, moderate inflation, and slowing GDP growth — the trend points toward continued strength in 2026. As the Federal Reserve maintains a softer monetary stance and the U.S. dollar weakens due to a persistent trade deficit, investors are expected to maintain high demand for gold as a hedge against both inflation and market uncertainty.

Under a base-case scenario, gold could rise roughly 10% over the year, placing prices in the $4,200–$4,300 range by the end of 2026. A stronger-than-expected slowdown in the U.S. economy or renewed geopolitical tensions could push gold even higher, while a surprise disinflation or rate hikes could temporarily limit gains. Overall, the fundamental backdrop remains supportive, suggesting gold will continue serving as a stable store of value amid a shifting global economic landscape.

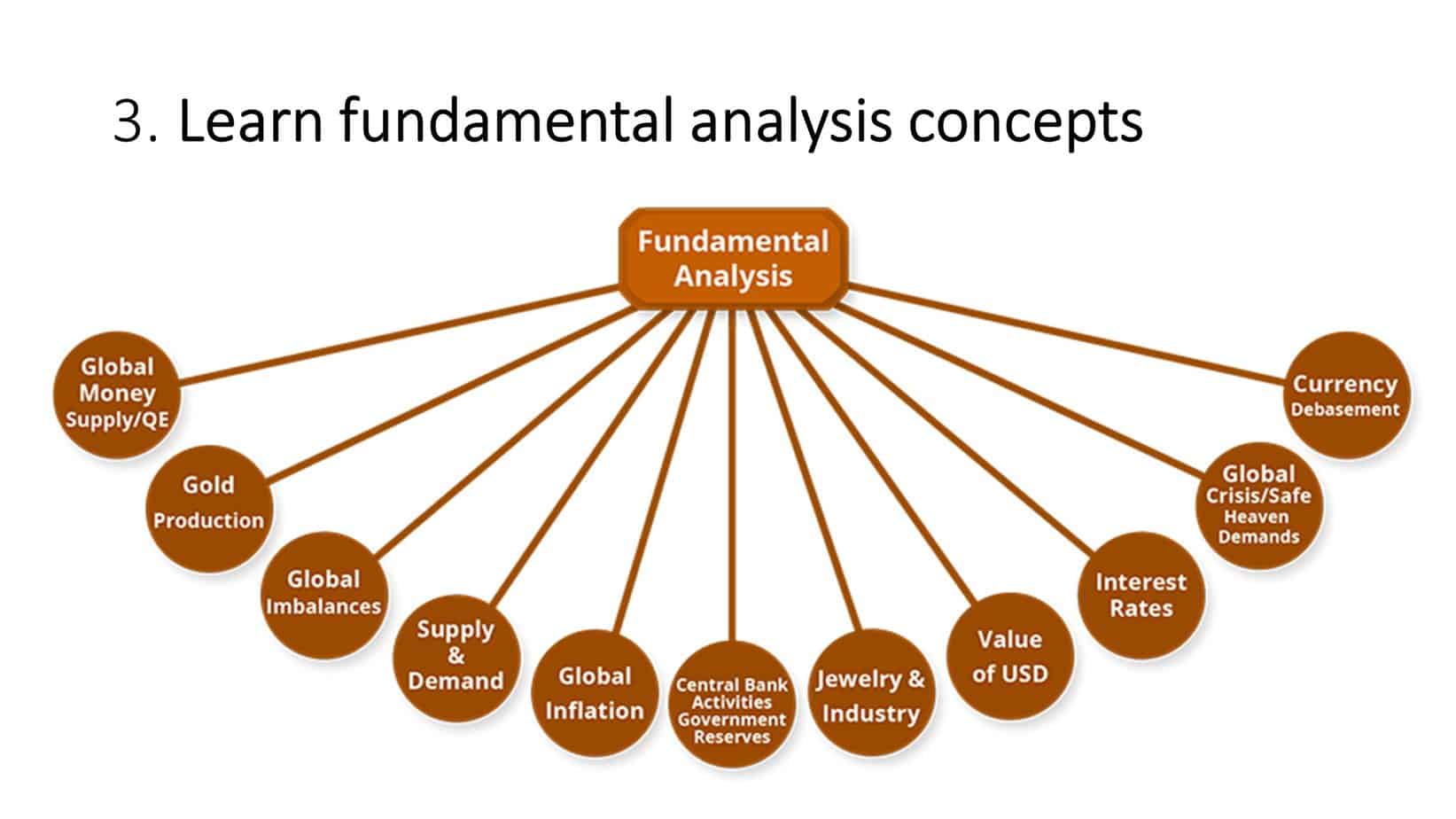

The rise of gold prices has significant fundamental economic impacts, both globally and domestically. Let’s break it down by the main areas of influence – based on theory:

1. Inflation and Monetary Policy

Gold often rises when inflation expectations increase or when central banks cut interest rates.

- Inflation Hedge: Investors buy gold to protect their purchasing power when currencies lose value due to inflation.

- Low Interest Rates: When real interest rates (interest minus inflation) are low or negative, holding gold becomes more attractive because it doesn’t yield interest but preserves value.

- Central Bank Behavior: Rising gold prices can signal that markets expect looser monetary policy or loss of confidence in fiat currencies.

Example: If the U.S. Federal Reserve starts cutting rates or signals that inflation is sticky, gold tends to surge as a hedge against dollar depreciation.

2. Currency Movements

Gold is priced in U.S. dollars, so its price has an inverse relationship with the USD.

- Weaker Dollar = Higher Gold: When the dollar weakens, foreign investors can buy more gold for the same amount of their currency.

- Stronger Dollar = Lower Gold: A strong USD makes gold more expensive for other countries, often reducing demand.

Thus, a rise in gold usually reflects a weaker dollar or a decline in global confidence in U.S. monetary stability.

3. Investor Sentiment and Risk Aversion

Gold is known as a “safe-haven asset.”

- During crises, wars, or market uncertainty, investors shift capital from risk assets (stocks, crypto) into gold.

- A rising gold price often reflects fear in the markets — investors expecting recessions, geopolitical tension, or financial instability.

In short, when risk rises, gold shines.

4. Impact on Commodities and Emerging Markets

- Commodities: Rising gold can lift other precious metals (silver, platinum) due to correlated demand for safe-haven assets.

- Emerging Markets: Gold imports can pressure trade balances and currencies in countries like India or Turkey, where gold demand is culturally strong.

A persistent rise in gold may increase import bills and worsen inflation in those nations.

5. Stock Market and Sector Implications

- Mining Stocks: Gold mining companies benefit from higher prices due to larger profit margins.

- Equities: Broad stock markets may fall if rising gold signals risk aversion or inflation fears.

- Bonds: Rising gold often correlates with falling bond yields, as investors seek protection from real yield erosion.

6. Central Bank Reserves and Global Trust

- Many central banks (like China, India, and Russia) have increased gold reserves to diversify away from the U.S. dollar.

- Rising gold prices strengthen the balance sheets of countries holding gold, increasing their monetary independence.

This can signal a shift in global financial power — away from fiat dominance toward tangible reserves.

In Summary:

| Indicator | Gold Rising Usually Means |

|---|---|

| Inflation Expectations | Increasing |

| Interest Rates | Likely to fall or remain low |

| U.S. Dollar | Weakening |

| Market Sentiment | Risk-off / Fear increasing |

| Global Confidence in Fiat | Decreasing |

| Commodity Sector | Bullish bias |

| Central Bank Behavior | Gold accumulation/diversification |

Would you like me to explain how rising gold affects forex pairs like XAUUSD or GBPUSD from a trading perspective (technically + fundamentally)? That would connect these fundamentals directly to your strategy.

Therefore, the weak US dollar, high interest rates (5.25% in May 2023), and recession impact the rising trend of the gold price.

See my projection a few years ago:

Any currency is given the back seat whenever global instability or turmoil occurs because precious metals take over. If we look back and review the market trends in 2012, when everyone believed that the world would end, gold prices reached a new high, and precious metals enjoyed a bullish market in the next year. History repeated itself in 2020, when gold became the first investment choice for many amidst the rising political and economic uncertainty.

Yellow metal became the preferred choice of those who were averse to risks and diversified their portfolios.

Is Silver Going Up to?

Gold and silver prices are strongly correlated, typically moving in the same direction because both are precious metals influenced by similar macroeconomic forces. When inflation expectations rise, real interest rates fall, or the U.S. dollar weakens, investors seek both metals as safe-haven assets, causing prices to climb together.

However, silver tends to show greater volatility — it rises faster in bull markets and falls harder in bear phases — because it has a larger industrial demand component (in electronics, solar panels, and batteries). In general, the gold-silver correlation coefficient has historically been around 0.80–0.90, meaning they move together about 80–90% of the time, with silver often amplifying gold’s trend rather than diverging from it.

However, silver prices are going up faster than gold. See video from last year:

Conclusion

In conclusion, gold’s strong performance in 2025 sets the stage for another bullish year in 2026, supported by easing monetary policy, falling real interest rates, and persistent global uncertainty. With the U.S. dollar likely to remain under pressure and investor demand for safe-haven assets staying firm, gold prices are expected to move steadily upward. The most probable scenario points to an average price range of $4,200–$4,300 per ounce by the end of 2026, confirming gold’s continued role as a reliable hedge against inflation and economic instability.

If you live in the US, you can invest in a Gold IRA and protect your retirement account from recession by investing in gold.

If you live outside the US:

He is an expert in financial niche, long-term trading, and weekly technical levels.

The primary field of Igor's research is the application of machine learning in algorithmic trading.

Education: Computer Engineering and Ph.D. in machine learning.

Igor regularly publishes trading-related videos on the Fxigor Youtube channel.

To contact Igor write on:

igor@forex.in.rs